When Brand Becomes a Value Lever: Five Critical Moments in M&A

When Brand Becomes a Value Lever: Five Critical Moments in M&A

How PE firms and leadership teams can use brand to protect, accelerate, and price enterprise value across the deal lifecycle.

The short version

Brand is one of the most underused levers of enterprise value in M&A. With roughly 92% of S&P 500 market value now tied to intangible assets [1][2], the soft stuff is the value. Five moments matter most — pre-close diligence, Day One, platform build, integration, and exit prep. Get them right and brand protects trust, accelerates synergies, and earns a premium at sale. Get them wrong and it quietly erodes the deal.

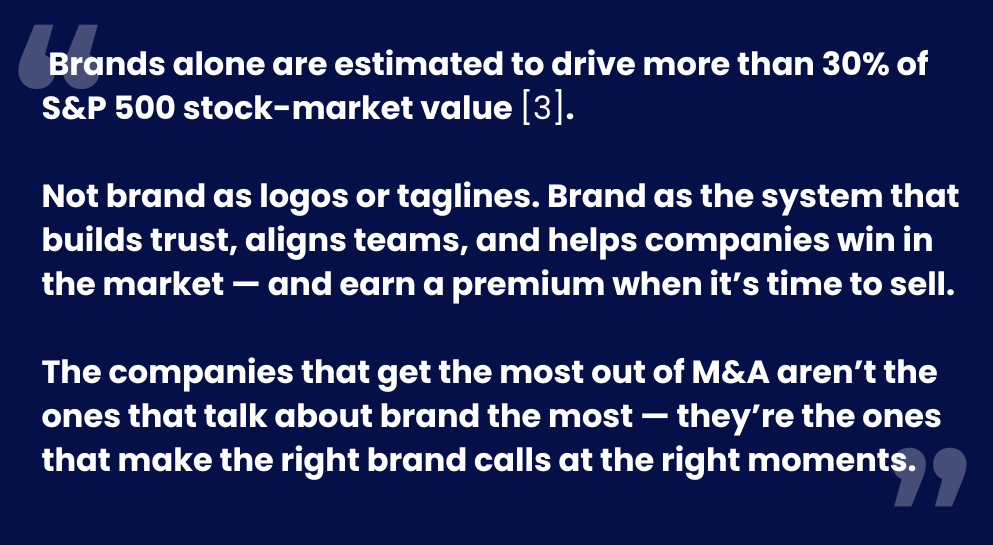

PE firms and leadership teams spend plenty of time on operations, finance, and growth. Fair enough. But one of the most powerful levers of enterprise value often sits right in front of them: brand. Intangible assets such as brand, intellectual property, software, and customer relationships now account for roughly 92% of the market value of S&P 500 companies, up from just 17% in 1975 [1][2]. Brands alone are estimated to drive more than 30% of S&P 500 stock-market value [3].

Not brand as logos or taglines. Brand as the system that builds trust, aligns teams, and helps companies win in the market — and earn a premium when it’s time to sell.

The reality? You don’t need a massive brand overhaul at all times. You need to get a handful of moments right. The moments when value is most at risk or most ready to grow. That discipline matters because the base rates are brutal: 70–90% of M&A deals fail or underperform on value creation [4][5], and KPMG found that 83% of mergers failed to enhance shareholder returns [6], often for reasons that never showed up in the spreadsheets. Across M&A work, five moments show up again and again.

Brand and M&A value: by the numbers

| Stat | What it measures |

| ~92% | Share of S&P 500 market value now tied to intangible assets such as brand, IP, and relationships — up from 17% in 1975. (Ocean Tomo) [1][2] |

| 83% | Mergers that failed to enhance shareholder returns. (KPMG) [6] |

| 70–90% | M&A deals that fail or underperform on value creation. (McKinsey; EY) [4][5] |

| 47% / 75% | Key employees who leave within one year / three years of a deal. (EY, Gallup via PeopleOne) [9] |

| +88% | Cumulative return of the strongest-brand portfolio vs. the S&P 500 since 2006. (Kantar BrandZ) [16] |

| 25–95% | Profit lift achievable from a 5-point increase in customer retention. (Bain) [7] |

Moment 1 — Pre-Close: Look Beyond the Numbers

Diligence is built to answer financial and operational questions. But many post-close surprises aren’t buried in spreadsheets, they’re sitting in customer perception. A business can look strong on paper and still be losing trust, relevance, or clarity in the market. On the flip side, some companies have real brand strength that hasn’t yet translated to performance.

What matters here isn’t rebranding, it’s reducing uncertainty. And brand signals are quantifiable enough to underwrite. Customer loyalty, for example, is a direct margin driver: Bain finds that a 5-point increase in retention can lift profit by 25–95%, because loyal “promoter” customers buy more, cost less to serve, and are measurably less price-sensitive [7][8]. A target’s loyalty base is a leading indicator of durable cash flow — or a hidden liability.

Focus on:

- Customer loyalty and preference — and whether it is concentrated or broad-based

- What actually drives buying decisions

- Reliance on founder reputation

- Brand compatibility across assets

- Customer and employee integration risk

Watch for:

- Mistaking strong revenue for strong brand

- Underestimating integration complexity

- Ignoring employee sentiment until it shows up the hard way. 47% of key employees leave within one year of a deal, and ~75% within three years, taking institutional knowledge and customer relationships with them [9].

Moment 2 — Day One: Create Confidence Fast

Right after close, everything is in motion. Customers want reassurance. Employees want clarity. Investors want momentum.

This is where a simple question becomes critical: what does this company stand for now? That answer shapes retention, recruiting, sales — everything that matters next. And the speed of that answer is a leading indicator of the whole deal. McKinsey’s study of 248 large deals found that 79% of acquirers who outperformed on shareholder return in the first 18 months were still outperforming three years later. Meaning—early momentum compounds [10]. The risk of moving slowly is just as concrete: acquirers that neglect the base business while chasing synergies typically see an 8% sales decline in the quarter after announcement [11].

You may need to define:

- Positioning for the standalone business

- Naming strategy

- Visual identity and communications

- Day-one messaging and internal rollout

Watch for:

- Treating brand as a “later” decision

- Changing too much (and losing equity)

- Leadership teams telling different stories

The best carve-outs don’t overcomplicate it. They create clarity, and fast. BCG reports that integrators who use the pre-close window to design the future company captured 9% more value from their deals than the market average [12].

Moment 3 — Platform Build: Make the Story Scalable

As platforms grow, complexity sneaks in. New products, new teams, new acquisitions — and suddenly the story stops holding together.

This is where brand stops being cosmetic and starts becoming infrastructure because it underwrites the kind of value modern PE actually depends on. Today, roughly 60–70% of private-equity value creation comes from EBITDA and revenue growth, not leverage or multiple expansion [13][14]. A coherent brand platform is what unlocks that growth: cross-sell, go-to-market efficiency, and pricing power. McKinsey finds that funds prioritizing operational and commercial value creation earn 2–3 percentage points higher IRR than peers [13].

Done right, a clear brand platform:

- Simplifies go-to-market

- Unlocks cross-selling

- Reduces confusion

- Strengthens hiring and retention

- Creates a coherent growth story

Watch for:

- Collecting brands without a system

- Letting each business tell its own story

- Treating culture and brand as separate lanes

At scale, brand isn’t just what you say — it’s how the whole organization behaves.

Moment 4 — Integration: Turn Assets Into an Enterprise

This is where value creation either compounds or stalls. Most integrations get the systems right. Fewer get the story right. Customers still see separate companies. Employees stay tied to legacy brands. And the promised synergies stay theoretical.

The data is unambiguous about where deals break: 50–75% of integrations fail to meet their objectives because of cultural clashes, and 76% of executives say cultural compatibility is a key determinant of integration success [15]. The cost of letting confusion linger is just as clear, by contrast, top acquirers capture about 50% of their committed synergy run-rate within the first year [10]. Brand and culture are not a separate workstream from synergy capture; they are the mechanism for it.

The real question: Are you building a portfolio or a company? Your answer should drive decisions about naming, architecture, positioning, and experience.

Watch for:

- Thinking org integration = market integration

- Moving too slowly (letting confusion linger)

- Moving too fast (breaking valuable equity)

- Leaving employees out of the story

The goal isn’t just scale. It’s a story that’s stronger than the sum of its parts.

Moment 5 — Exit Prep: Tell the Right Story Before Buyers Do

By the time a sale process starts, most teams are ready on financials. Brand? Not always. That’s a miss, because buyers aren’t just buying the past. They’re underwriting the future.

And the future is exactly what a strong brand makes credible. Over the long run, the companies behind the strongest brands have delivered a +88% cumulative return versus the S&P 500 (and +251% versus the MSCI World Index) since 2006 [16][17]; a McKinsey analysis similarly found that strong-reputation brands generate 31% more shareholder return than the MSCI World average [3]. A credible brand narrative is what makes future growth — the part buyers pay a multiple for — believable rather than aspirational.

A strong brand story answers the questions they really care about:

- Why has this company won?

- What makes it different?

- How durable is that advantage?

- Where does future growth come from?

Watch for:

- Waiting until the CIM is underway

- Relying on internal assumptions

- Leading with features instead of advantage

The best exit narratives don’t spin the truth — they make it undeniable.

Final Thought: Brand Is Not a Side Workstream

Brand doesn’t sit next to value creation. At its best, it accelerates it and in a world where about nine-tenths of enterprise value is now intangible [1][2], it increasingly is the value. The companies that get the most out of M&A aren’t the ones that talk about brand the most — they’re the ones that make the right brand calls at the right moments.

The question isn’t whether brand matters. It’s whether it’s helping value grow — or quietly getting in the way.

Frequently Asked Questions

Does brand really affect M&A deal value?

Yes. Intangible assets — including brand — now make up roughly 92% of S&P 500 market value, up from 17% in 1975 [1][2], and brands alone are estimated to drive more than 30% of S&P 500 stock-market value [3]. Companies with the strongest brands have outperformed the S&P 500 by +88% since 2006 [16].

Why do so many M&A deals fail?

Studies consistently put the failure or underperformance rate at 70–90% [4][5], and KPMG found 83% of mergers failed to enhance shareholder returns [6]. Culture and integration are leading causes: 50–75% of integrations miss their objectives due to cultural clashes [15], and 47% of key employees leave within a year of a deal [9].

When in the deal lifecycle should brand be addressed?

At five moments: pre-close diligence, Day One, platform build, integration, and exit prep. Acting early matters — acquirers that design the future company before close capture about 9% more deal value [12], and those who plan integration during diligence outperform on both speed and value.

How does brand support value creation in private equity?

Roughly 60–70% of PE value creation now comes from EBITDA and revenue growth rather than financial engineering [13][14]. A clear brand platform unlocks that growth through cross-sell, go-to-market efficiency, and pricing power, and funds that prioritize this earn 2–3 points higher IRR [13].

Sources

- Ocean Tomo, “Ocean Tomo Releases 2025 Intangible Asset Market Value Study Results,” 2025. https://oceantomo.com/insights/ocean-tomo-releases-2025-intangible-asset-market-value-study-results/

- Ocean Tomo, “Intangible Asset Market Value (IAMV) Study.” https://oceantomo.com/intangible-asset-market-value-study/

- Siegel+Gale, “Brand Value ROI: The Case for Brand Investment Through Strategic Metrics” (citing The Economist and McKinsey). https://www.siegelgale.com/brand-value-roi-the-case-for-brand-investment-through-srategic-metrics/

- McKinsey & Company, “The Importance of Cultural Integration in M&A: The Path to Success.” https://www.mckinsey.com/industries/oil-and-gas/our-insights/the-importance-of-cultural-integration-in-m-and-a-the-path-to-success

- EY, “How Culture Can Unlock M&A Performance.” https://www.ey.com/en_uk/insights/workforce/how-culture-can-unlock-m-a-performance

- PMIStack, “Post-Merger Integration Statistics” (citing KPMG). https://pmistack.com/blog/post-merger-integration-statistics

- Bain & Company, “The Economics of Loyalty.” https://www.bain.com/insights/the-economics-of-loyalty/

- Loyalty Economics, retention and loyalty ROI research. https://www.loyaltyeconomics.org

- PeopleOne, “How Culture Can Make or Break Your Merger and Acquisition Integration” (citing EY/Gallup and Deloitte). https://www.peopleone.io/resources/blogs/how-culture-can-make-or-break-your-merger-and-acquisition-integration/

- McKinsey & Company, “Post-Close Excellence in Large-Deal M&A.” https://www.mckinsey.com/capabilities/m-and-a/our-insights/post-close-excellence-in-large-deal-m-and-a

- McKinsey & Company, “A McKinsey Perspective on Value Creation and Synergies” (Merger Management Compendium). https://www.mckinsey.de/~/media/McKinsey/Business%20Functions/Organization/Our%20Insights/Merger%20Manager%20Compendium/A%20McKinsey%20perspective%20on%20value%20creation%20and%20synergies.pdf

- BCG, “Post-Merger Integration.” https://www.bcg.com/capabilities/mergers-acquisitions-transactions-pmi/post-merger-integration

- McKinsey & Company, “Value Creation: The Impact Counts, Not the Plan.” https://www.mckinsey.com/uk/our-insights/uk-blog/value-creation-the-impact-counts-not-the-plan

- Moonfare, “5 Examples of Private Equity Value Creation.” https://www.moonfare.com/blog/5-examples-pe-value-creation

- Financier Worldwide, “Culture Clashes in M&A: New Perspectives.” https://www.financierworldwide.com/culture-clashes-in-ma-new-perspectives

- Kantar, “Using Kantar BrandZ to Make the Case for Long-Term Brand-Building Investment.” https://www.kantar.com/inspiration/brands/using-kantar-brandz-to-make-the-case-for-long-term-brand-building-investment

- Kantar BrandZ, “Charting 20 Years of Brand Value: Kantar BrandZ 2025 Ranking.” https://www.prnewswire.com/apac/news-releases/charting-20-years-of-brand-value-kantar-brandz-2025-ranking-reveals-the-worlds-most-valuable-brands-302456367.html

- WIPO, “Intangible Assets” (using Brand Finance data). https://www.wipo.int/en/web/intangible-assets